Related Authors

-

Benjamin Graham Investor

Benjamin Graham Investor -

Joel Greenblatt Manager

-

Charlie Munger Business person

-

Mohnish Pabrai Investor

-

David Einhorn Hedge fund manager

-

Warren Buffett Investor

-

Bill Ackman Hedge fund manager

-

Walter Schloss Investor

-

David Tepper Manager

-

Peter Lynch Businessman

-

Bruce Greenwald Professor

-

Ray Dalio Businessman

-

Daniel S. Loeb Manager

-

Jeremy Grantham Investor

-

Whitney Tilson Author

-

-

-

James Chanos Manager

-

John Paulson Manager

-

Carl Icahn Businessman

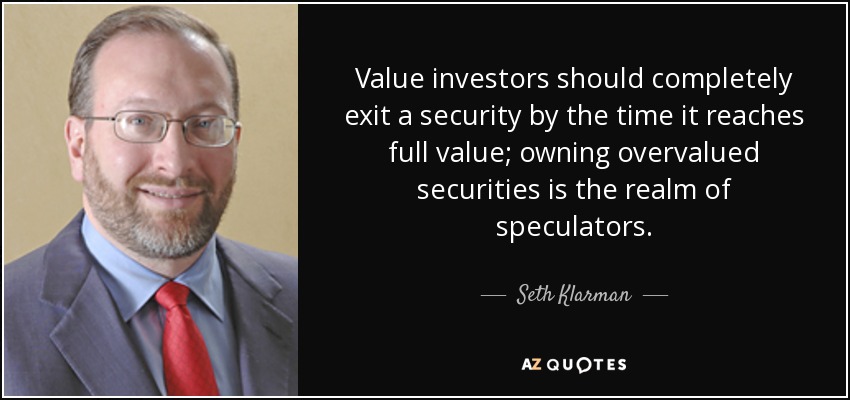

Seth Klarman

- Born: May 21, 1957

- Occupation: Author

- Cite this Page: Citation